Vikram is 36, a senior engineer at a Bengaluru product company, earning ₹22L a year. By most measures, he's doing everything right. Zerodha account — active. Kuvera SIPs — running. FD in HDFC — parked. SGB from 2019 — sitting somewhere. A 2BHK in Pune — purchased five years ago. Some jewellery gold from his wedding. LIC policy he barely remembers.

Last December, his wife asked a simple question before they started planning a house upgrade: "How much are we actually worth right now?"

Vikram spent two hours trying to find out. He opened Zerodha. Then Kuvera. Then the HDFC netbanking FD page. He called his dad about the gold. He guessed at the flat's current value. He added it all in a notes app. The total felt wrong — either too high or too low, he couldn't tell.

This isn't a discipline problem. It's a tooling problem. No single app speaks all the asset languages a middle-class Indian investor uses in 2026.

The app overload trap

Here's what Vikram's financial life actually looks like spread across platforms:

- Zerodha — INFY, TCS, RELIANCE direct stocks ₹4.8L

- Kuvera — Parag Parikh Flexi Cap SIP ₹6.2L

- HDFC Netbanking — FD maturing in 4 months ₹5.0L

- CDSL / RBI — SGB Series VII (2019) ₹1.8L

- Jewellery box — Gold from wedding, ~180g ₹?

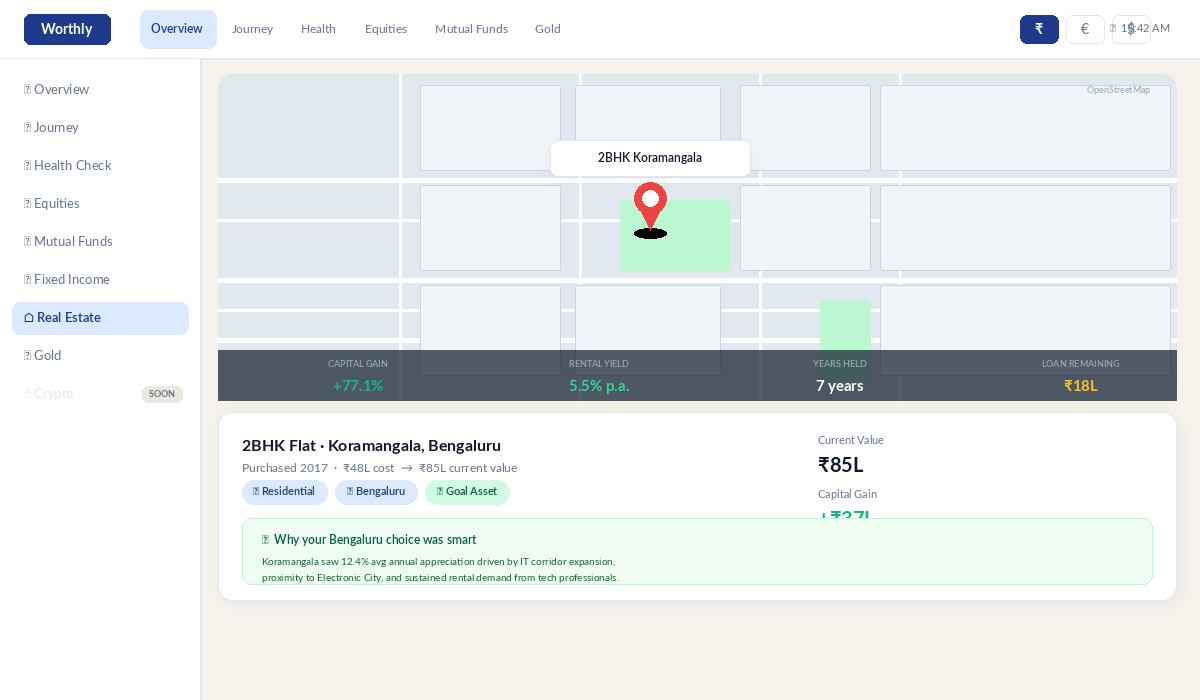

- MagicBricks estimate — 2BHK Pune, Wakad ₹68L?

Each number is real. None of them talk to each other. None of them update in real time. And none of them add up to one coherent answer.

What actually broke the pattern

Vikram's colleague mentioned Worthly in a Slack thread about personal finance tools. He was sceptical — he'd tried Money View, ET Money, and INDmoney before. All of them either wanted his broker login credentials or only tracked one or two asset classes properly.

Worthly was different in one specific way: it handles the complete mix. Not just stocks and mutual funds, but FDs with maturity dates, SGB with the 8-year lock-in, physical gold at live MCX spot prices, real estate with capital gain calculation, PPF — all in one session, all in INR, all at live prices.

He entered everything once. It took about 20 minutes — stocks by ticker, mutual funds by AMFI search, FD balance and maturity date, SGB units and issue date, the gold weight, the flat's purchase and estimated current value. Then he clicked Calculate.

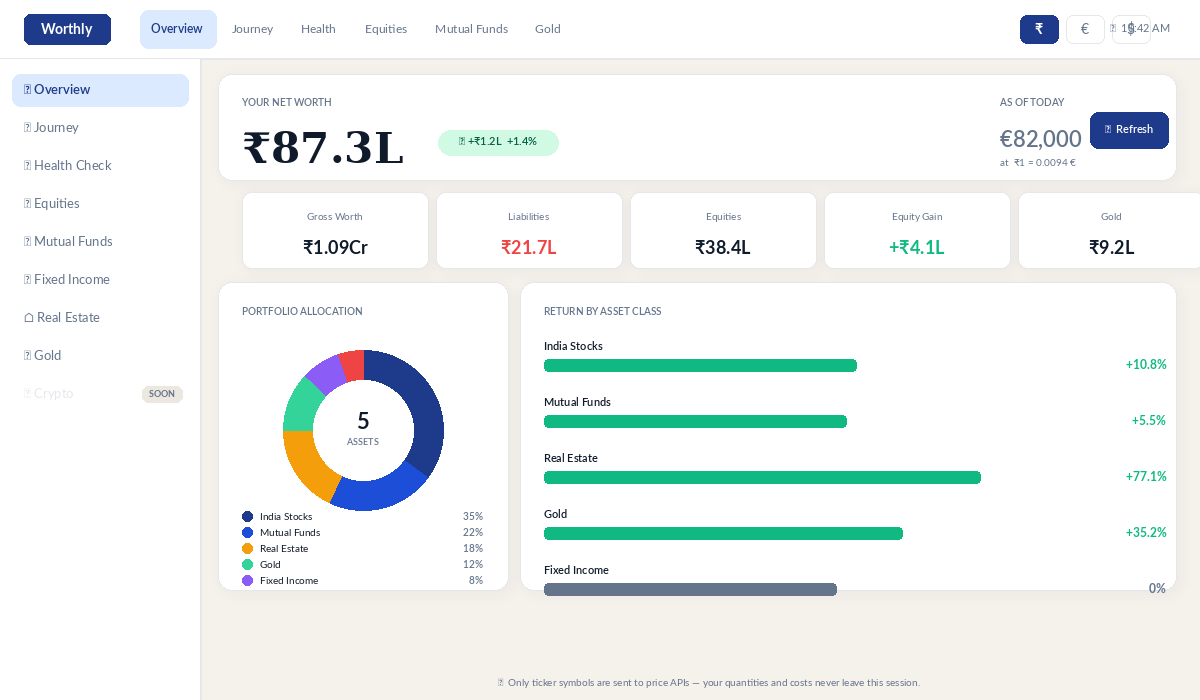

The number at the top: ₹87.4 lakhs. His first honest net worth figure. Not a guess, not a sum of stale screenshots — live prices for everything that has a live price, manual for everything that doesn't.

The things he didn't know he didn't know

The dashboard number was useful. But two other things surprised him more.

First: the FD alert. The app flagged that his HDFC FD was maturing in 4 months — he'd completely forgotten. That ₹5L was about to roll over at a lower rate unless he actively renewed or redirected it. A ₹5 lakh decision he would have missed entirely.

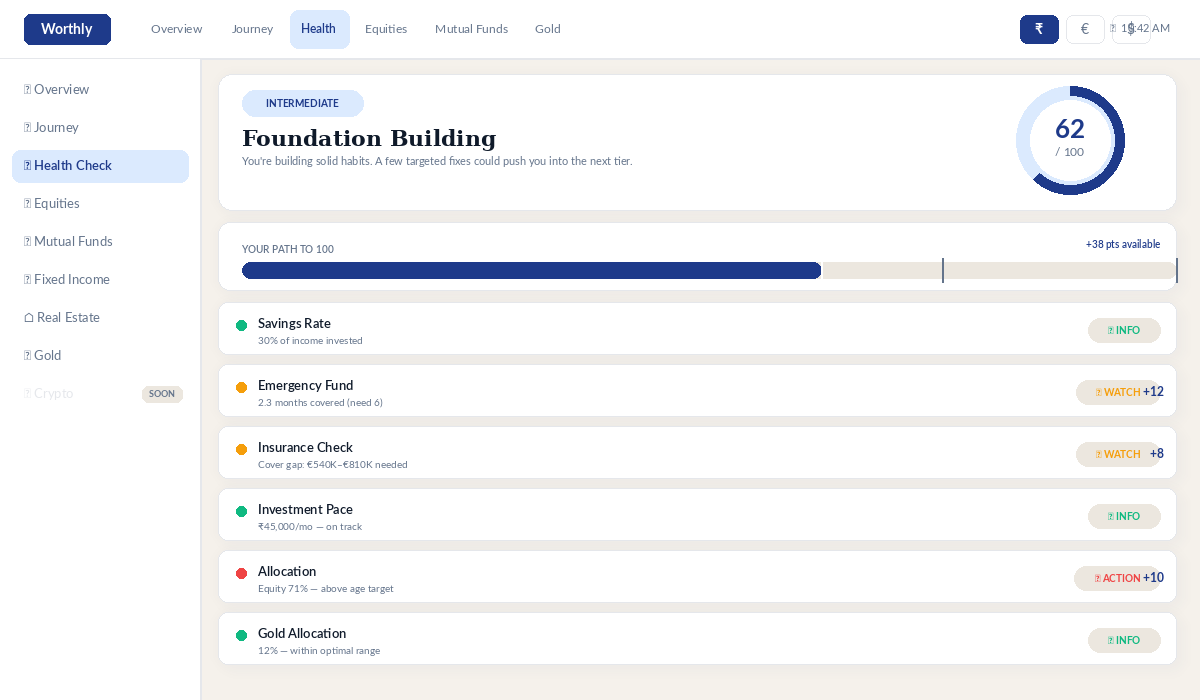

Second: the Health Check score. He got 58 out of 100. The score broke down into components — emergency fund (he had 2.1 months, not the recommended 6), savings rate (18%, below the 30% flag threshold), insurance adequacy (term cover gap), allocation drift (82% of his investable assets in equities, well above the age-appropriate band), and gold (slightly over-allocated at 14% including jewellery).

None of these were surprises in isolation. He knew his emergency fund was thin. He knew his equity allocation was heavy. But seeing it scored — with specific gaps and specific fixes — made it actionable in a way that a vague sense of "I should probably do something" never was.

What it tracks that no other app does

The privacy question

Vikram's main hesitation with INDmoney and ET Money had been the same: they wanted to read his SMS inbox or connect to his broker account to pull data automatically. He didn't love the idea of a third-party reading his transaction history to build a profile.

Worthly doesn't do any of that. You enter your own numbers. No broker connection. No SMS access. No credentials. The only external calls are price lookups — your ticker symbols go out, live prices come back. Your portfolio itself never leaves your session. When you log out, it's gone from the server. You save it by downloading a JSON file to your own device.

For a lot of people that trade-off — slightly more setup, complete data privacy — is exactly the right one.

Where it actually helps most

For NRIs juggling multiple currencies across borders, Worthly solves a currency problem. For someone like Vikram — living in India, earning in rupees — the problem it solves is different: consolidation and clarity.

The average Indian investor in 2026 has money in at least 4–5 places — direct stocks, SIPs, FD, gold (physical or SGB), and often real estate. Every individual piece is managed reasonably well. But nobody is looking at all of it together and asking: am I on track? Is my allocation sensible for my age? Is anything about to expire that I've forgotten about?

That's what Worthly answers. One number, one health score, one view.

Vikram re-ran the calculation last week, three months on. The number had moved to ₹91.2L — driven mostly by the Parag Parikh fund and a good run in TCS. His health score had improved to 63 — he'd moved ₹1.5L from his savings into a liquid fund to patch the emergency fund gap.

The upgrade conversation with his wife took about 10 minutes. They had a number they trusted. The decision was straightforward.

Know what you're actually worth — every asset class, live prices, one number.

Try Worthly free →First 3 sessions include full PRO features. No credit card. No broker login. No data stored.